2024-04-16

2024-04-16

Interpret the statement that SBTi can use Environmental Attribute Certificates (EAC) to reduce Scope 3 emissions

Author: Xu Shuaijun (Carbon Emission Reduction System Alliance, sole responsibility for the article)

The statement issued by SBTi on April 9 did not include the methods and schedule for implementing EAC, but it has caused a lot of controversy and speculation in the industry. The author interprets the statement based on his personal understanding and hopes to answer the concerns of relevant people.

Question1. What is the background and origin of this statement? What is the definition of Environmental Attribute Certificate (EAC)? Will internal employee protests have any effect?

This statement is a resolution passed by the Board of Trustees. Since WRI, CDP, WWF, UN Global Compact and other mainstream NGOs are members of the SBTi Board of Trustees, these NGOs will fully support this statement.

SBTi has been investigating companies’ use of EAC as climate emission reduction targets since September 2023. (The cover of the research document is as follows)

In the survey document, SBTi defines the categories of EAC as follows:

Environmental attribute certificates can include:

Next, we explain the two main reasons why SBTi increases the use of EAC as a Scope 3 emission reduction method:

(source: https://carboncredits.com/)

In short, despite the opposition and dissatisfaction among SBTi employees. The resolution of the Board of Trustees is the general trend and this statement should continue to be implemented.

Question 2. SBTi What kind of carbon rights will be recognized (Emission reduction credits)?

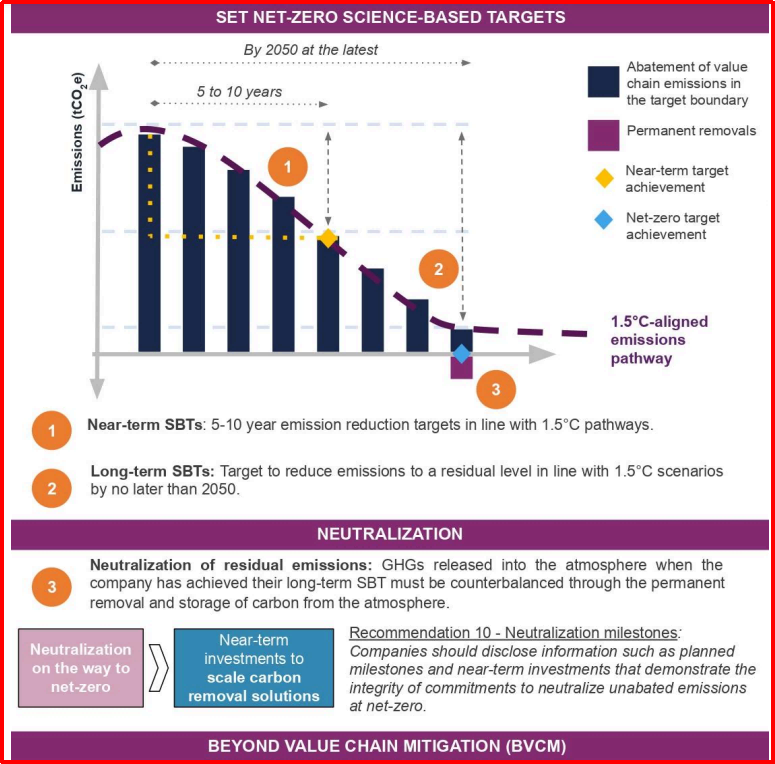

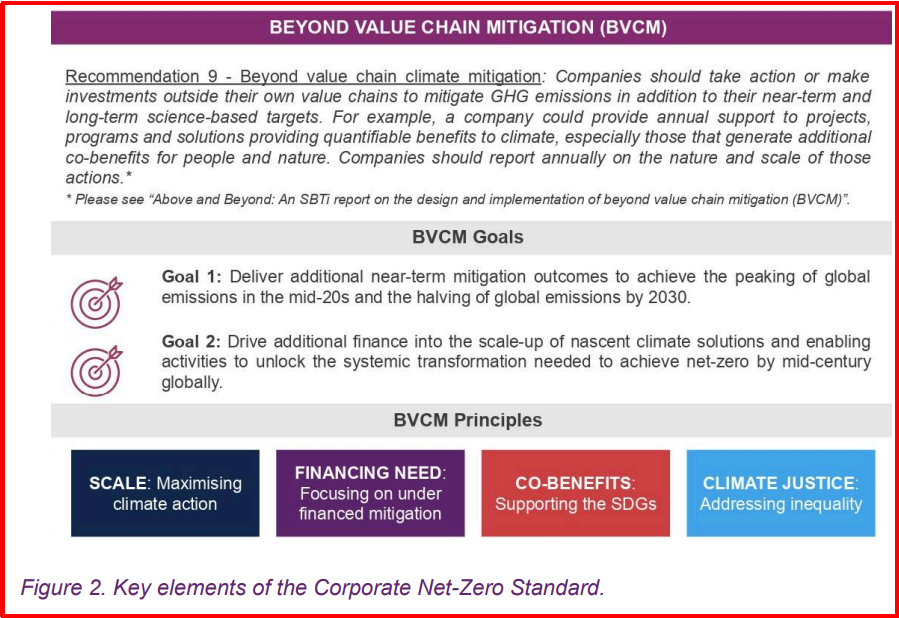

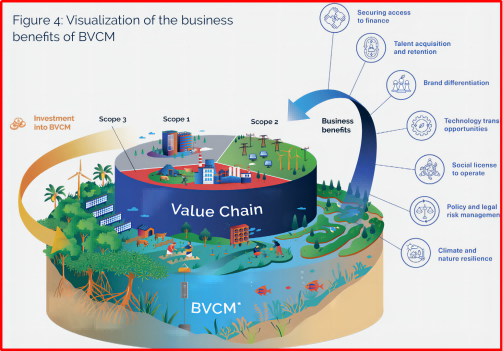

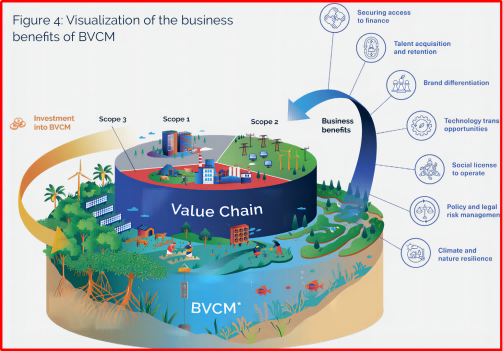

In addition to carbon rights, the EAC categories planned by SBTi already have rigorous and mature regulations and verification systems internationally and in the European Union. What everyone has doubts about is what kind of carbon rights will SBTi recognize? Please review the new content of SBTi’s series of standards and guidelines to deduce the answer to question 2. In the net-zero standards released by SBTi in March 2024, the part that reduces emissions outside the value chain (Beyond Value Chain Mitigation-BVCM) has been clearly included as a recommended requirement. As shown in the figure below, how to use the carbon rights recognized by SBTi to promote emission reduction has become a non-mandatory part of SBTi’s new net zero standard. It is also one of the key elements of the so-called net zero standards.

When updating the net zero standards, SBTi also released the “ABOVE AND BEYOND: AN SBTI REPORT ON THE DESIGN AND IMPLEMENTATION OF BEYOND VALUE CHAIN MITIGATION (BVCM)” guide, explaining the principles, conditions, methods and mechanisms for using carbon rights outside the value chain. . The guide also clearly explains the relationship between internal and external emission reduction methods in a graphical way.

Because the SBTi BVCM Guide quotes the Voluntary Carbon Market Integrity Initiative (VCMI) regulations and guidelines as many as 57 times. So it is obvious that SBTi will adopt the requirements and regulations of VCMI to recognize voluntary carbon rights.

Please refer to the regulations of VCMIVCMI-Claims-Code-of-Practice-November-2023.pdf (vcmintegrity.org),No explanation is given here. The conclusion is that the regulations and requirements of VCMI are very strict, and the industry’s carbon rights approval agencies (Gold Standard, Verra, etc.) are working hard to improve their approval requirements and verification requirements to comply with VCMI regulations. Therefore, carbon rights recognized by SBTi as Scope 3 emission reduction methods will not be accused of so-called greenwash.

As for Taiwan’s current self-regulated carbon rights mechanism and Gold Standard, Verra’s regulations already have a very large gap and cannot be in line with international standards. Not to mention meeting the requirements of SBTi and VCMI. Don’t get your hopes up.

question3. When to implement?How to implement?

SBTi estimates that a draft version of the corresponding new standard will be released soon in July 2024. Since most technical issues can be based on VCMI regulations, SBTi has to decide what percentage is allowed to be used to meet Scope 3 emission reduction targets. The problem is relatively simple.

What are your predictions? It will be implemented at the end of 2024, and the usage shall not exceed 10%-20% of the Scope 3 annual emission reduction target?

A related issue is that, like SBTi and VCMI, in order to verify emission reduction claims and effects, companies that use carbon rights to reduce emissions will be required to pass emission reduction target verification. VCMI has issued its Monitoring Reporting and Assurance (MRA) regulations, and it is estimated that SBTi will also issue Monitoring Reporting Verification (MRV) regulations in mid-2024, requiring companies to carry out the process of implementing emission reduction targets after passing target recognition (validation). verify.

Question 4. Impact on enterprises implementing SBTi

Due to various reasons, companies will probably need to verify the process of implementing emission reduction targets this year?

Finally, a joke. In the past, the author has always been against investing in voluntary carbon rights (even high-quality and high-standard ones). Based on SBTi’s statement, the position is somewhat different.

Are there still questions you’d like to see clarified? Or do you need to communicate? please contact General consultation: Carbon Emission Reduction System Service Alliance (crssa.com.tw).

Interpret the statement that SBTi can use Environmental Attribute Certificates (EAC) to reduce Scope 3 emissions

The Carbon Reduction System Service Alliance (CRSSA) was officially established! We are committed to becoming the best partner for enterprises to expand internationally and move towards net-zero carbon reduction.

Select [GHG Protocol accounting rules and its test

Carbon Reduction System Service Alliance (CRSSA)